Streamlined Compliance

We handle your finance, tax, and legal compliance, letting you focus on growth. Our experts deliver audits & filings to safeguard your success.

Streamlined Compliance

We handle your finance, tax, and legal compliance, letting you focus on growth. Our experts deliver audits & filings to safeguard your success.

About

We Have Decades of Cross-Functional Experience in Finance, Legal & Compliance

At KMG, we are more than just consultants — we are your trusted growth partners. With deep domain expertise across finance, taxation, law, and audit, our dedicated team supports businesses, investors, and startups in navigating complex regulatory and operational landscapes.

Multi-disciplinary Expertise (CA, CS, Lawyers, MBAs)

Proven Track Record with Startups, VCs, & Enterprises

Transparent, Strategic, and Execution-Focused

Compliance-Driven, Outcome-Oriented Approach

Our Clients

Service

What Service We Offer

Due Diligence Services

Click to view

Service

What Service We Offer

Due Diligence Services

Click to view

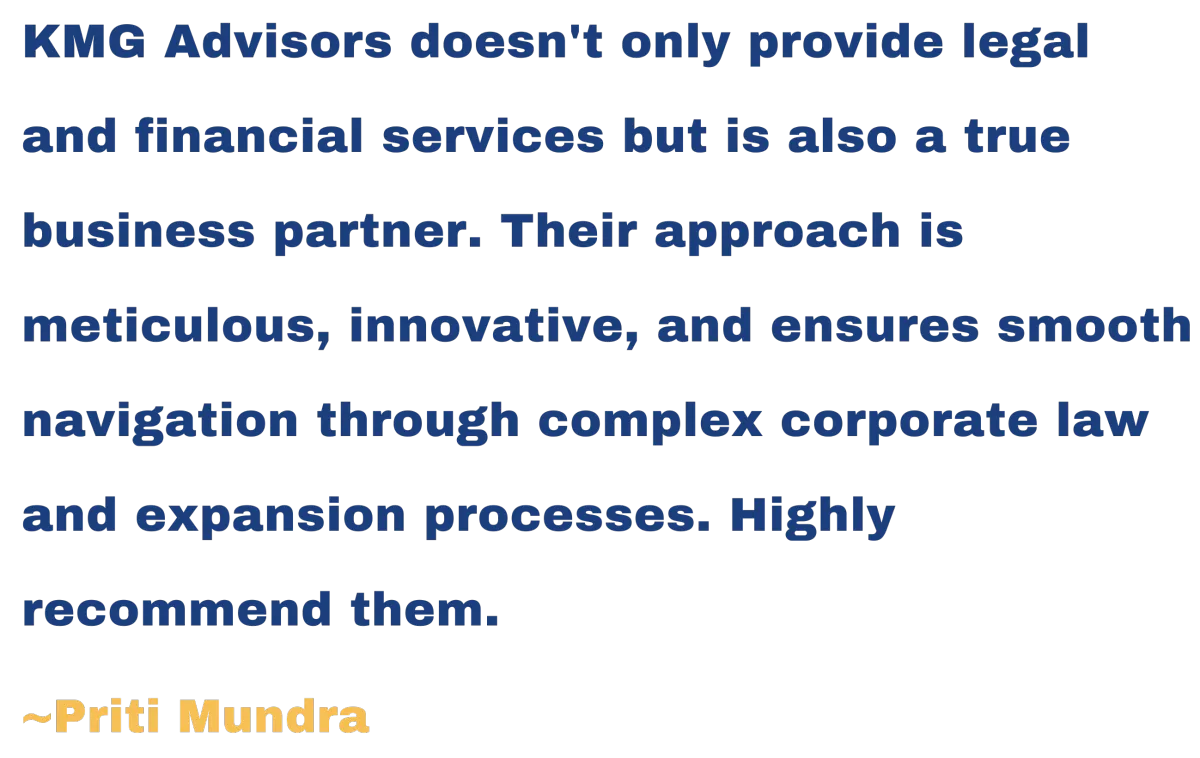

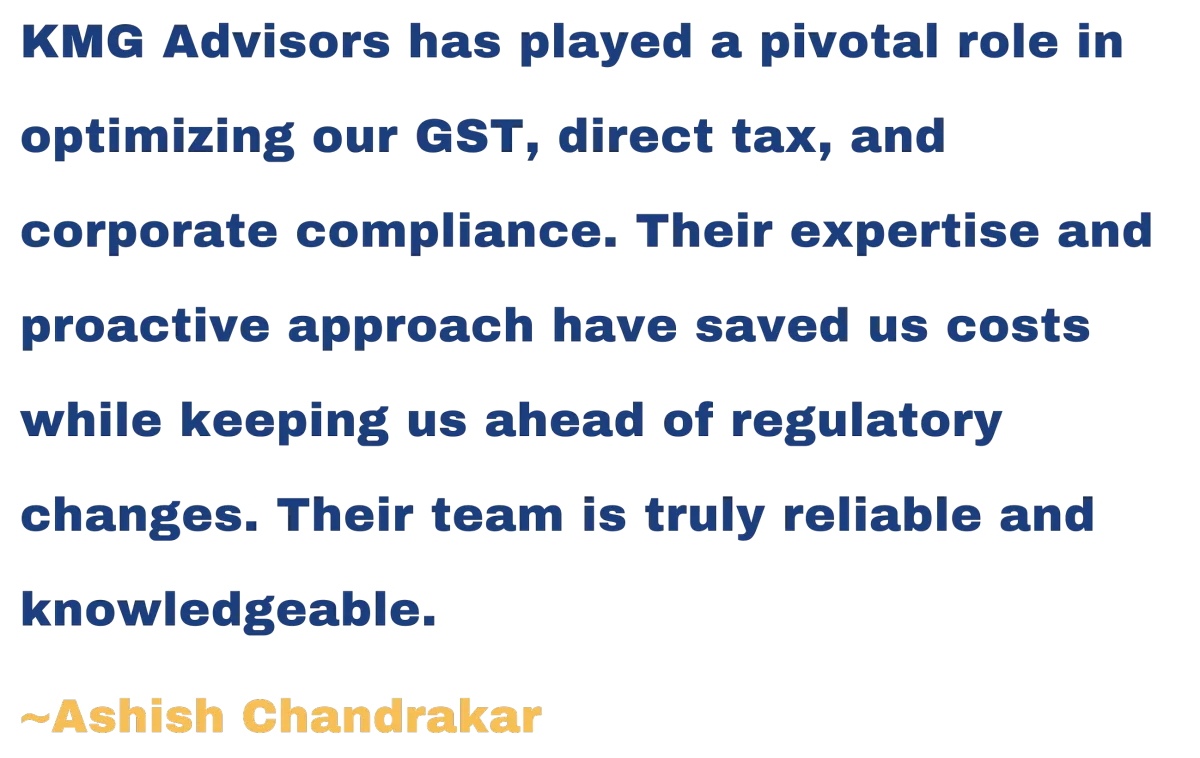

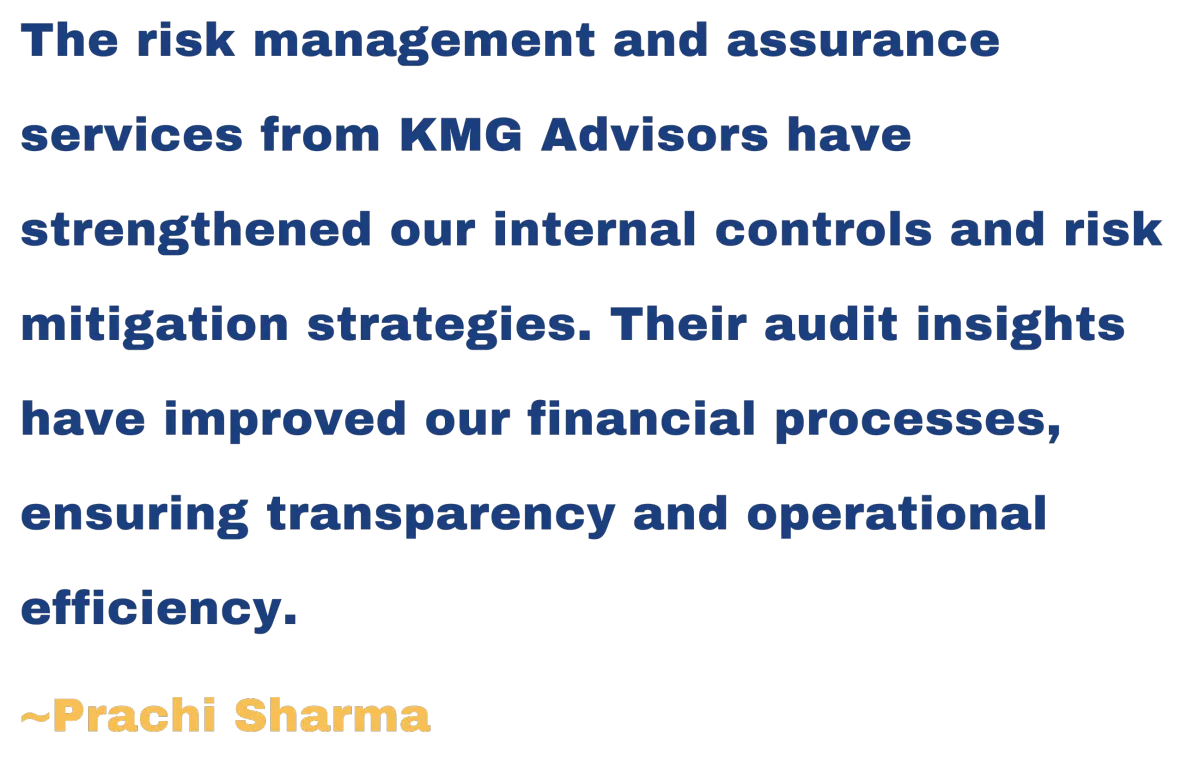

Testimonials

Trusted by Startups, Investors & Enterprises

Across India and Beyond

FAQS

What services do you offer?

Comprehensive financial services—from bookkeeping and tax planning to compliance and personalized advice—designed for individuals and small businesses.

How much do your services cost?

Our pricing is flexible and based on your needs. Get in touch for a personalized quote and transparent cost breakdown.

How do you ensure the security of my financial data?

We prioritize your data security with cutting-edge protection, strict compliance, and ongoing staff training—ensuring your information stays safe and confidential.

Our Team

Meet Our Professional Team

Gallery

GANESH KANODIA

Co-Founder & Director

(Taxation Head)

(B.Com, FCA)

Ganesh Kanodia, a Chartered Accountant, holds 10+ years of experience in GST and Income Tax advisory, litigation, and tax planning. Leads due diligence for fund raises and strategic deals. Known for financial insights and stakeholder trust, he also teaches at NGO events and study circles across India, contributing to knowledge-sharing and industry growth.

PRASHANT KUMAR GUPTA

Co-Founder & Director

(Legal and Secretarial Head)

(BSc, FCS, LLB)

Prashanth Kumar Gupta, Company Secretary and law graduate, brings over a decade of experience in legal advisory, M&A, and compliance. He is well-versed in SEBI, FEMA, POSH, and NCLT matters. Prashanth also mentors future professionals as a visiting faculty at ICSI, offering deep insights in corporate law, governance, and regulatory frameworks.

RAHUL GUPTA

Risk & Assurance Head

(B.Com, FCA)

Rahul Gupta, a Chartered Accountant with 10+ years of experience, specializes in statutory, internal, and transfer pricing audits, along with risk management. He is adept in finance and tax due diligence, especially for high-growth digital and e-commerce businesses. Also serves as a visiting faculty for NGOs and study circles across India, contributing to industry learning and development.

SHARAD MAHESHWARI

Co-Founder & Director

(B.Com, FCA)

Sharad Maheshwari, a Chartered Accountant with 10+ years in direct tax, specializes in tax planning, advisory, and compliance for individuals and businesses. Skilled in international taxation, he enables global tax efficiency. Sharad regularly teaches at respected institutes, enhancing understanding of complex tax systems across India.

GANESH KANODIA

Co-Founder & Director (Taxation Head)

(B.Com, FCA)

Ganesh Kanodia, a Chartered Accountant, holds 10+ years of experience in GST and Income Tax advisory, litigation, and tax planning. Leads due diligence for fund raises and strategic deals. Known for financial insights and stakeholder trust, he also teaches at NGO events and study circles across India, contributing to knowledge-sharing and industry growth.

PRASHANT KUMAR GUPTA

Co-Founder & Director

(Legal and Secretarial Head)(BSc, FCS, LLB)

Prashanth Kumar Gupta, Company Secretary and law graduate, brings over a decade of experience in legal advisory, M&A, and compliance. He is well-versed in SEBI, FEMA, POSH, and NCLT matters. Prashanth also mentors future professionals as a visiting faculty at ICSI, offering deep insights in corporate law, governance, and regulatory frameworks.

PRASHANT KUMAR GUPTA

Risk & Assurance Head

(B.Com, FCA)

Rahul Gupta, a Chartered Accountant with 10+ years of experience, specializes in statutory, internal, and transfer pricing audits, along with risk management. He is adept in finance and tax due diligence, especially for high-growth digital and e-commerce businesses. Also serves as a visiting faculty for NGOs and study circles across India, contributing to industry learning and development.

SHARAD MAHESHWARI

Co-Founder & Director

(B.Com, FCA)

Sharad Maheshwari, a Chartered Accountant with 10+ years in direct tax, specializes in tax planning, advisory, and compliance for individuals and businesses. Skilled in international taxation, he enables global tax efficiency. Sharad regularly teaches at respected institutes, enhancing understanding of complex tax systems across India.

Get In Touch

Address: 211 Second Floor, Star Towers, Silokhra Rd, Block A, Sector 30, Gurugram, Haryana 122022